Introduction

What is the future of the Artificial Intelligence (AI) industry? Which AI products will take the lead, and which AI companies will reap the rewards? Will open-source or closed-source models be used the most, and why? The question “what AI will be able to do?” has been thoroughly discussed, but less time has been spent considering which specific capabilities will dominate and which will fade into obscurity. This brief seeks to apply a theoretical framework from economics for understanding the future of the AI industry. I differentiate AI-powered products into four categories, build a cost and demand framework for AI firms, gather evidence supporting the framework, and consider six implications for the industry and broader economy.

- Content making AI products, like Sora, will continue to be shuttered

- AI will lower barriers for creation but raise barriers for dissemination

- Cash-rich companies will outlast their rivals, and a concentrated oligopoly of AI companies will remain in each niche

- Companies risk overbuilding AI infrastructure due to sustained loss-leading strategy

- Open-source models will be a large component of future AI use for productivity tools

I consider the case where Artificial General Intelligence (AGI) or Superintelligence (ASI) is not developed. The path of AI capabilities is assumed to be incremental improvements from current frontier models. If AGI or ASI is developed, most economic theory and models are no longer applicable as cognitive labor is no longer a necessary resource in production. It is unclear whether an economy with AGI or ASI would continue to serve human ambitions. As such, I assume AI models cannot operate responsibly or successfully entirely without human intervention and fulfilling human needs remains the primary purpose of the economy.

Theoretical Framework

Differentiating AI products

Hank Green, a YouTuber, author, and entrepreneur, published a video—following the shuttering of all OpenAI video generator services—titled “What is “Slop” (and why it gives me hope)” (vlogbrothers 2026). Green explores why certain types of AI-generated content on the internet have been deemed ‘slop,’ which is characterized as “shoddy or unwanted A.I. content in social media, art, [and] books” (Hoffman 2024). Green details how certain AI-produced products, such as videos on social media, are deemed as slop not only because it requires lower effort, but also since the prevalence of the content leads to decreased perceived value. Slop is content that is so plentiful and “so easy to make, it no longer feels worth watching” (vlogbrothers 2026).

To illustrate Green’s observations, imagine your social media feed of choice, except every post you see is a random draw of all the content posted on the platform in the last year. After seeing how many low quality and similar, possibly AI-generated, posts would you start incurring negative utility from the experience? Would you pay to have the content filtered for you? The demand to filter out unwanted content has been persistent since the internet enabled global information flows and individuals became overwhelmed with said information. Long before AI-generated videos, social media platforms implemented recommendation algorithms to sort through the hundreds of hours of content uploaded every minute. The outcome of these algorithms is that viewership is concentrated among the most engaging and prestigious content. Filtering algorithms are necessary and highly demanded since there is negative utility from being overwhelmed with low-quality and undifferentiated content (Bawden and Robinson 2020). The value of low-quality undifferentiated content rapidly drops off after a few videos in the genre. As such, the perceived value of all content, and especially content produced by AI, is prestige-dependent.

The other type of AI product is one that can provide stable utility by completing a job. Unlike slop, the products doing a job, henceforth referred to as tools, have enduring perceived value even as AI has made it more efficient or entirely automated. For example, Python code written by AI is not perceived by most to be valued less than code written by humans if the code is the same in quality. This dichotomy of tools and content is a key dimension for differentiating AI products. Tools have stable perceived value as supply increases since their use-value is preserved, whereas content has diminishing perceived value driving willingness to pay down faster through two quantity channels.

In addition to considering tools versus content, AI products can also be differentiated into final goods and capital goods. Final goods are products consumed by the end-user, such as food. Capital goods are products used by producers to produce final goods, such as a tractor. There are many AI products that are final goods, such as Google’s AI summary for search, and many AI products are capital goods, such as Claude Code or Cowork.[1] This dimension is important to consider because the customers and business models for final and capital goods are fundamentally different. For instance, businesses are fewer in number and conduct larger transactions than consumers, businesses tend to spend longer than consumers considering each purchasing decision, and business and household decision-makers are reached through different channels. Table 1 summarizes the four types of AI products based on the two dimensions, provides examples of each type of tool, and summarizes the long-run outcome of the sector.

Table 1: Four types of AI products.

| Tools (stable perceived value) | Content (diminishing perceived value) | |

| Final goods (consumed by an end-user) | Utility tool e.g. search, chatbot, autonomous cars Outcome: oligopoly or monopoly of highly profitable direct-to-consumer services | Prestige-dependent good (slop) e.g. movies, TV, art, books, music, social media posts Outcome: controlled production and gatekeeping become more valuable (barriers to entry are not lowered) |

| Capital goods (used by producers) | Productivity tool e.g. coding tool, Cowork, design, customer service Outcome: oligopoly or monopoly of highly profitable business-to-business services | Slop-maker e.g. video generation, image generation Outcome: limited sustainability and profits, depends on differentiation of output |

Theory of the AI Tools Firm

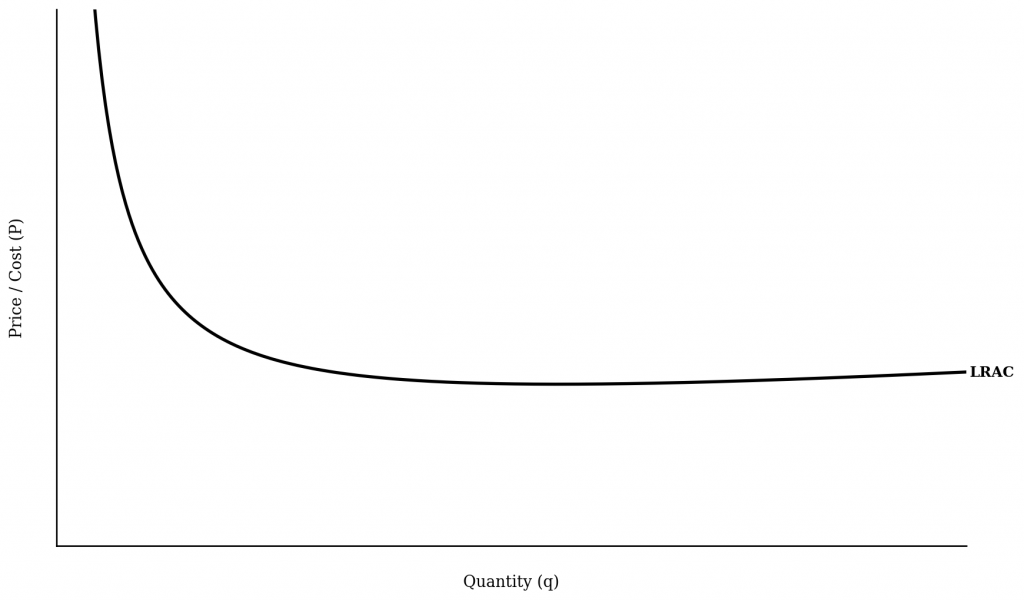

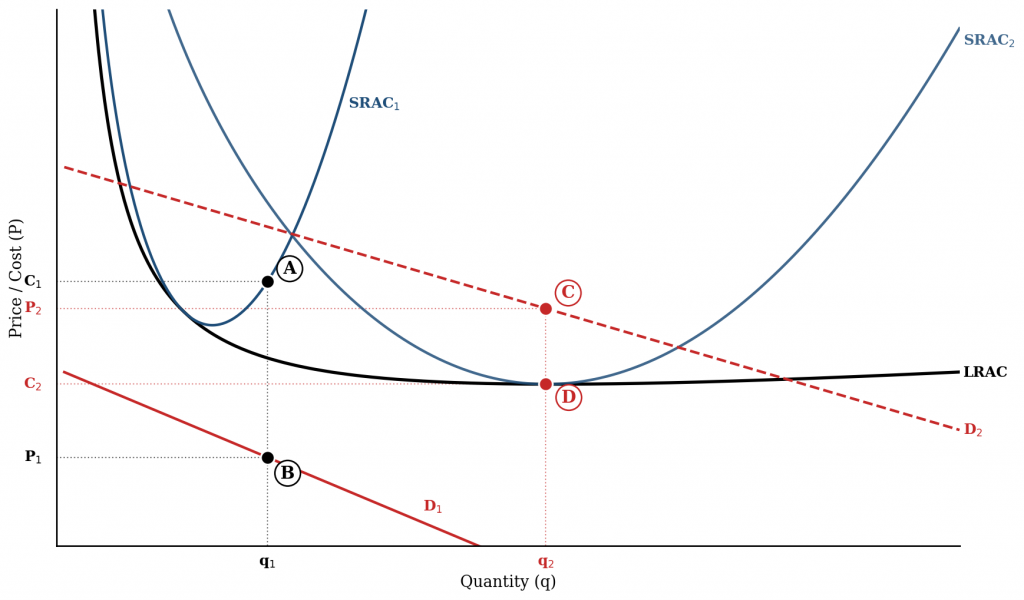

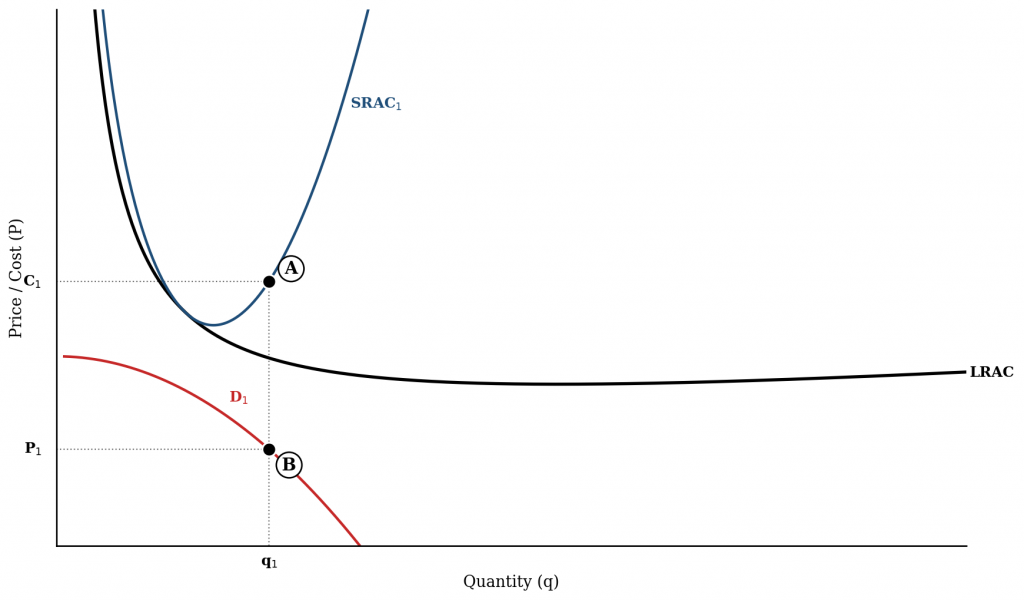

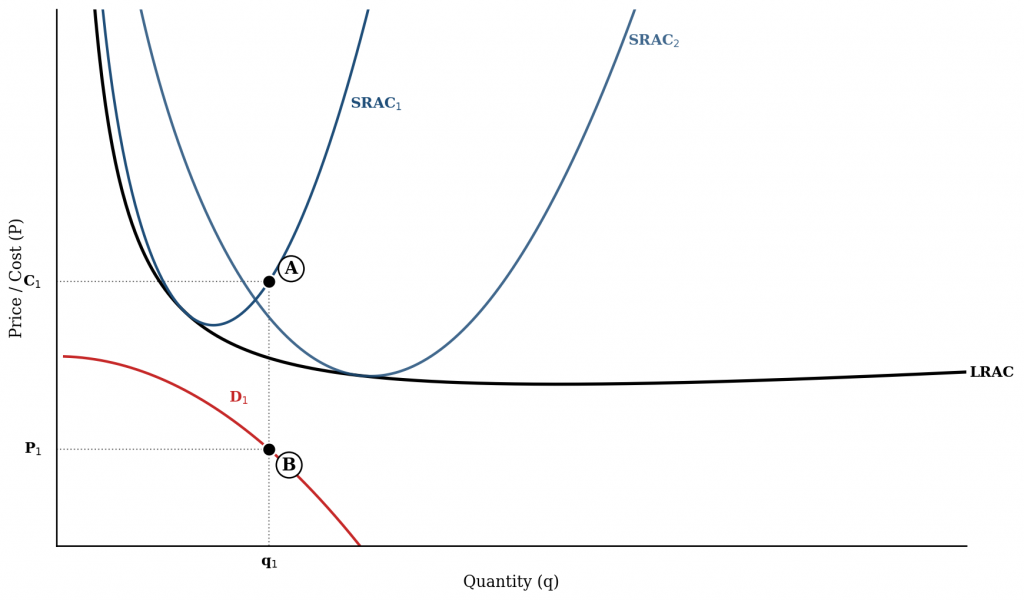

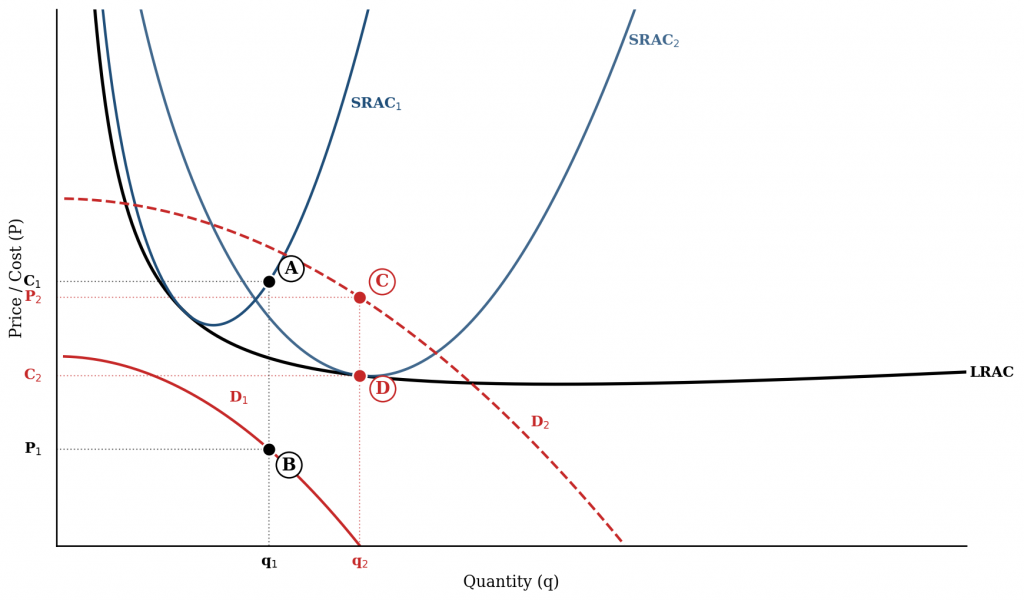

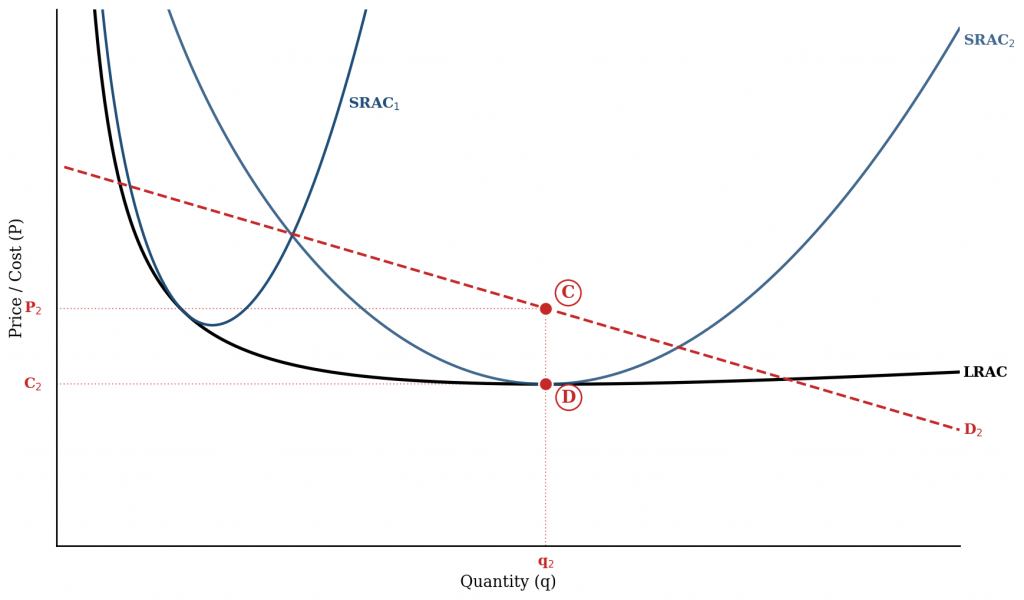

The theory of the firm is a standard model in the field of economics for describing the behavior of firms and I apply it first to a closed-source frontier model AI tools firm. First, we’ll start with the Long Run Average Cost curve (LRAC). The LRAC displays the cost of providing the AI service per unit sold. The LRAC is a minimum cost boundary assuming all optimizations are realized over several years. The AI industry using closed-source frontier models has high fixed costs from training a model and acquiring the scalable infrastructure to provision a service, with relatively low variable costs to provide the next person the same service; there are economies of scale. For example, Claude Code has enormous development costs (fixed costs) but its operation (variable costs) is relatively cheap. As such, unit costs are high at low quantities and quickly decrease as the quantity supplied increases and the initial fixed cost investment is spread over many more units sold. After a certain quantity of provisioning AI services, frontier models face resource constraints raising the cost of providing the service. Strained water supplies (a limited resource) and opposition from local populations and politicians can raise the cost of developing AI infrastructure after a certain quantity. These limitations are reflected in a slight increase in the LRAC at high quantities

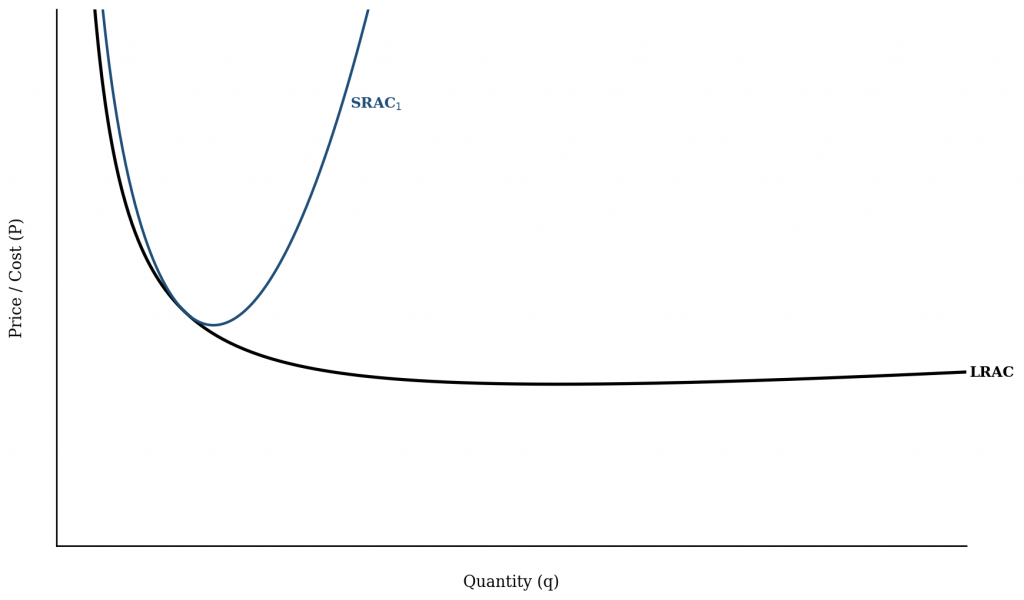

Second, we add a Short Run Average Cost curve (SRAC1). The SRAC1 curve displays the cost of providing the AI service per unit sold, but with limitations on resources. Even at very high costs, there is only a certain amount more product that can be produced due to lacking the inputs. To illustrate, over the course of 1 year, a hypothetical AI company spending $10 billion may be able to increase their capacity by 10% by purchasing more existing data centers at increasing prices, but over 5 years the same spending could increase their capacity by 50% through building more data centers and acquiring the additional capacity at a more reasonable price.

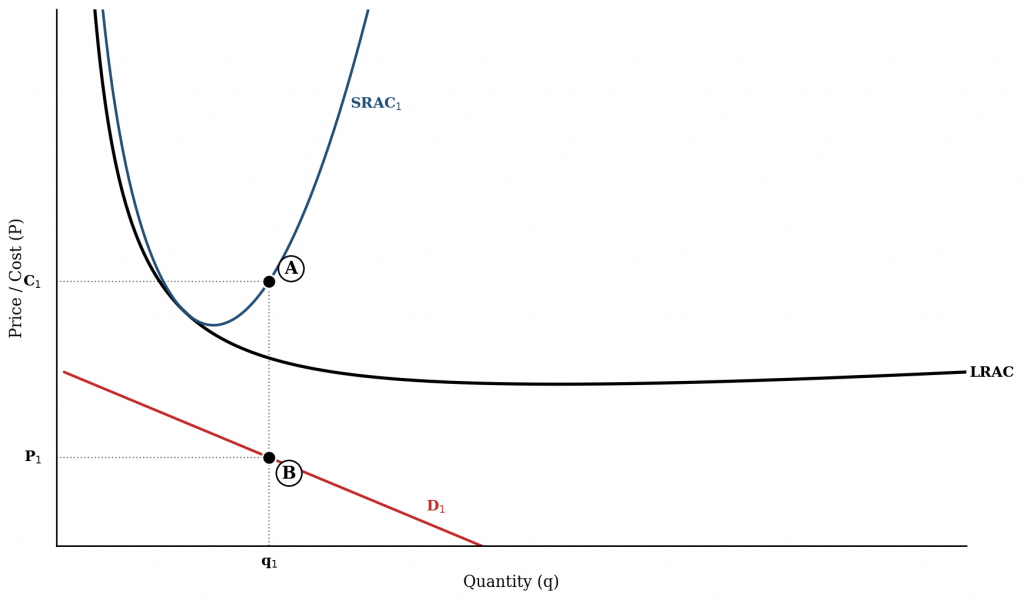

Third, we can now add our demand curve (D1). The demand curves which model how many of the AI product consumers would want to purchase and at what price they would be willing to pay. I use a downward-sloping linear demand curve for AI tools, assuming an even distribution in willingness to pay. The standard demand curve can be used for tools since they have stable perceived value so the increased provision of the good does not disproportionately affect demand for the good.

Now, let’s discuss the intersections between the curves and what it means. Today, firms in the AI tools industry have costs SRAC1 and face demand from consumers at D1. Firms are choosing to use loss leader strategies, providing consumer with cheap capital subsidized services in the short-term. Each firm is choosing to provide the quantity of services q1. Drawing a straight line up at this quantity, the intersection point A with the cost curve determines the price of C1 and the intersection point B with the demand curve sets the price P1. Notably, the cost is far higher than the price, so the firm is losing money on each transaction. The total loss is the difference between the price and cost multiplied by the quantity.

Loss-leading has been employed by a range of companies including OpenAI who had a reported operating loss of $9 billion in 2025, and the company projects continued losses up to $74 billion in 2028 (Smith 2025). Of their over 900 million weekly active users, around 850 million are free users (Backlinko Team 2026). Why are companies engaging in loss-leader strategies? In a growing market with high long run industry attractiveness, it is worthwhile for investors and companies to enter aggressively for the purpose of forcing rivals out of the market and gaining greater profits for years or decades to come. Incumbent firms, such as Google and Microsoft, also have the need to invest in the new disruptive technology for fear of being overtaken and replaced. As said by Alphabet (Google) CEO Sundar Pichai, “the risk of under-investing is dramatically greater than the risk of over-investing” (The Economist 2024).

Now, let’s turn to what happens in the future. Over several years, a few key changes will occur:

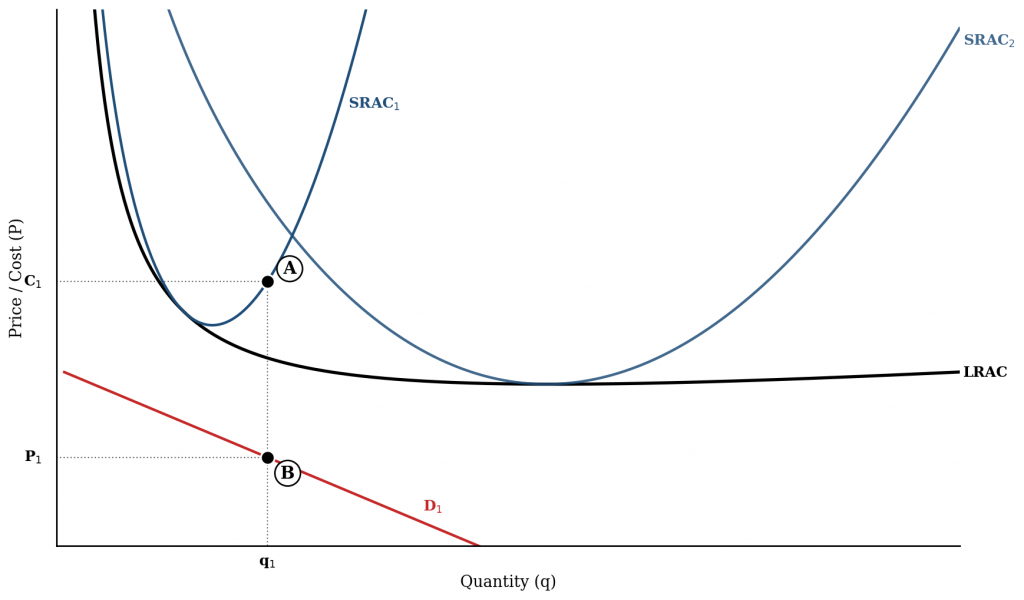

- Resources for provisioning AI (computer chips, power, etc.) will have time to catch up and temporary cost crunches will ease. This moves SRAC along LRAC to the right where unit costs decrease but more quantity can be provided.

- Demand for AI products from companies and individuals may naturally grow. More consumers and businesses become aware of AI products and engage in adopting them, a process that takes time to refine. This shifts the D curve to the right as more AI products are demanded.

- Loss-leading from a few companies pushes their competitors out of the market. The D curve is the demand for a single firm’s products. Therefore, reduced competition shifts the D curve further to the right as each company will receive a larger share of the AI demand.

The new equilibrium points are where firms produce at a quantity of q2. Once again, drawing a straight line up the price is now set at point C, raised from P1 to P2; costs are set at point D, reduced from C1 to C2. Since price is now above cost, the firm is profitable earning the difference between the price and cost multiplied by the quantity. This completes the model for the AI tools firm. The loss-leading strategies currently employed by firms is captured by the model, and firms anticipating increases in demand and lower costs stand to gain significant future profits from temporary cash burning.

How are AI content products different?

Theory of the AI Content Firm

While costs for generating AI content are higher than generating text, this change in the cost is not the most relevant difference for our model, as it simply shifts the cost curves upward. For simplicity, we can keep the cost curves from previous AI tools model.

In contrast to AI tools firms, AI content firms face a different demand curve. An increasingly downward sloping curve needs to be used to reflect the decline in perceived value as the quantity provisioned increases. The decline in perceived value pushes demand towards zero at which point the good is entirely slop and unwanted. Slop can cause a negative price if its presence is unwanted and causes a disutility for the consumer. In this case, products and systems that remove slop will become valuable. The same dynamic of loss-leading for longer term profits occurs, however the potential for future profits is far smaller while the temporary loss is roughly the same. The differences in the demand for AI content vs. AI tools illustrates how the AI tools industry is more attractive.

Similar to the AI tools case, drawing a straight line up at quantity q1, the intersection point A with the cost curve determines the price of C1 and the intersection point B with the demand curve sets the price P1. The cost is higher than the price, so the firm is losing money on each transaction.

Looking ahead several years, first, costs for AI content subside as capacity is improved like AI tools costs. The SRAC curve shifts right.

Second, demand may increase as more people become aware of the products and the industry consolidates further. This shifts the demand curve to upwards and rightwards as well. Drawing a straight line up the price is now set at point C, raised from P1 to P2; costs are set at point D, reduced from C1 to C2. Unlike in the AI tools scenario, the AI content firm faces a smaller window of productivity due to the increasingly downward sloping shape of the demand curve. The amount of profit is likely to be smaller than for AI tools as the quantity sold (market size) is capped by declining consumer appetite for AI content.

One additional problem specific to AI content is maintaining the reputation and preventing devaluation. If all the companies in the industry through adopting the loss-leading strategy overshoot the optimal quantity and cause AI-generated content to be devalued, the price of AI content may be sticky at the devalued negative price. For example, if the loss-leading occurs for long enough that systems for filtering out slop are implemented by platforms, it is hard to imagine that the systems would be removed after a reduction in quantity of slop as the norm that the content is unwanted has been set. In this situation, the demand curve would remain at D1 or below regardless of competitor exits from the market, making the entire industry unsustainable as there is no opportunity for price to be above cost. Furthermore, returning to AI content cost issues, the AI models for image or video generation are far costlier than text models, which may further increase the gap between demand and cost, decreasing profitability. These two factors increase the attractiveness of AI tools compared to AI content.

The case where a slop-making product is sustainable would be when it is closer to a productivity tool and its output is used to create a differentiated utility tool; essentially if it is not used to create slop. For example, Midjourney’s image generation service is smaller and profitable, targeting more professional paid users only who use Midjourney for “early stages of creative workflows” (Kayman and Segal 2025). Arguably, while Midjourney engages in image generation, its usage profile falls closer in line with productivity tools than slop-makers.

Impact of open-source AI models

The availability of open-source AI, through platforms such as OpenRouter and products powered by these cheaper models may reduce demand for closed-source frontier models, depending on whether they are valid substitutes for the frontier models. Open-source models are free to access so users are not paying for the intellectual property associated with a frontier model. Combined with their cheaper operating costs, open-source models introduce a significant amount of cost competitiveness into the industry. Open-source models are also not far behind the frontier. According to an index of benchmarks, the open-source Kimi K2.6 performs only slightly below closed-source Gemini 3.5 Flash and above Claude Sonnet 4.6 (Artificial Analysis, n.d.).

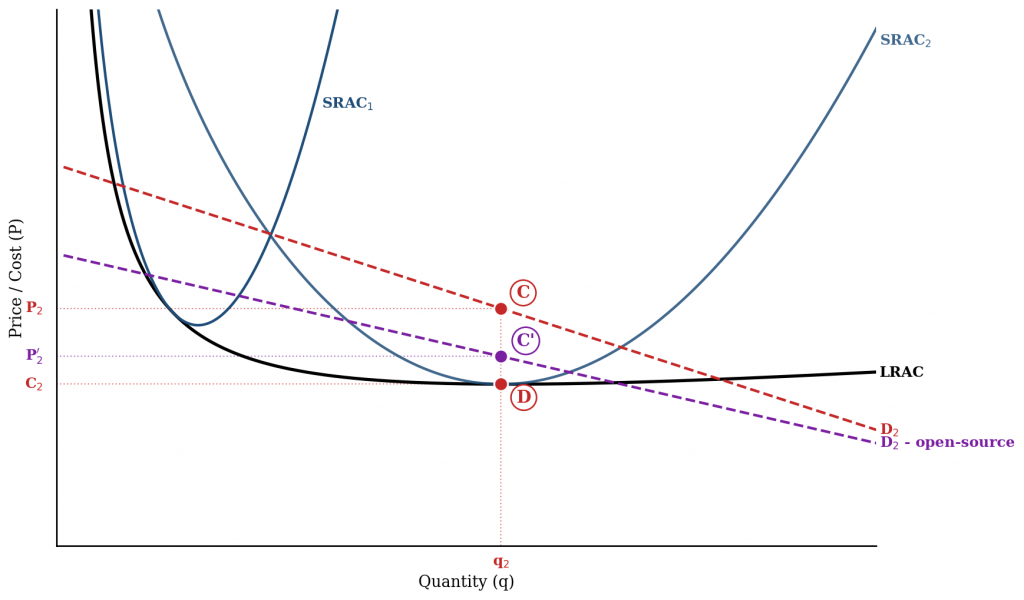

Here is our model only in the long term at time 2. We see the price setting point at C and the cost point at D, resulting in substantial profits for the frontier firms.

Given the acceptable performance of open-source models and possibly diminishing utility from better frontier models, it is likely that open-source models will squeeze demand for frontier models downwards in the long run several years from the present. This shifts the demand curve down as shown by the shift from the red D2 curve to the purple D2 – open-source curve. The reduced demand results in a decreased price equilibrium point going from point C to C’, and price decreases from P2 to P2’. This results in reduced profitability for the frontier providers as the difference between price and cost has narrowed.

Summary of theory of the AI firm

From today (time 1) to several years in the future (time 2), trends in the AI sectors predicted by the economic framework are as follows:

| Trend for AI Tools Firms | Trend For AI Content Firms | |

| Quantity | Increases | Could increase, but risk of overshooting quantity and causing devaluation during loss-leading |

| Price | Increases | Could increase, but risk of staying low |

| Cost | Decreases | Decreases |

| Profits | Increases | Could increase but less than AI tools and risk of staying unsustainable |

Indeed, we can already observe some of the changes occurring. Some AI companies are shifting towards raising prices or raising ad revenue at the expense of the user. OpenAI and Google announced ads in ChatGPT and Gemini (Proton 2026; Google Business 2026). Other companies, such as Anthropic, are experimenting with reducing usage limits, which also increases the unit price of AI queries to the consumer (Béchard 2026). OpenAI had a $1 billion investment deal with Disney and planned to license over 200 characters for use in its video generation platform, Sora (Jin 2026). Instead on March 24, 2026, OpenAI discontinued Sora along with all video generation products on their other platforms and Disney’s $1 billion investment was wound down. OpenAI cited that their priorities were in other areas, and they are recognizing how tools gain more profits in the long run.

Implications for the AI industry and beyond

1. Slop-making products, like Sora, will continue to be shuttered

Our model predicts that AI tools will be more profitable than AI content in the long run. Additionally, there are substantial risks that AI content will not be profitable at all if restrictions or filters designed to remove AI content are implemented. For AI firms with the flexibility to choose their investments, each dollar and compute second spent on AI content and slop-making capital goods is a dollar/compute second not spent on developing the more profitable AI tools. Given this dynamic, most frontier AI companies are likely to move away from slop-making products as their cost structure is worse and not sustainable in the long run.

2. AI will lower barriers for creation but raise barriers for dissemination

A common marketing message for AI products is that they will lower barriers of entry for creation, enabling users to make ideas a reality without the need to develop the previously necessary skills. While this may be true for the process of creating a work, AI does not increase a work’s likelihood of dissemination or success for prestige-dependent goods. As the market is flooded with slop, it will be devalued and create value in mechanisms that filter it out. This is reflected in the history of algorithmic filtering of low-quality content and in the increasingly downward slope of our AI content demand curve. Raising barriers to publishing and dissemination, such as by conducting AI authenticity checks or extensive expert review processes, will be more valued in a world with more slop. The final result from these forces will be that barriers for dissemination are raised and even higher quality will be the standard.

3. Cash-rich companies will outlast their rivals, and a concentrated oligopoly of AI companies will remain in each niche

Barriers to entry in the AI industry are incredibly high and the industry is attractive in the long run. Therefore, cash-rich incumbents are incentivized to use loss-leader strategies to force rivals out of the market to gain greater market share and long run profits. Companies that have more cash will be able to loss-lead for longer than their low cash competitors, driving them out of the market. The cash-rich companies that remain can then capture the greater shift to the right in the demand curve and greater profits shown by the model. An exception is if companies decide to tacitly collude, raising prices together and avoiding a sustained loss-leading price war.

4. Companies risk overbuilding AI infrastructure due to sustained loss-leading strategy

AI companies are currently engaged in loss-leading strategies to gain market share. The model predicts that there are currently more firms in the AI industry than there will be in the future and each of them is engaged in producing a quantity beyond their profitable levels. When there are more firms today than in the future and each firm is overinvesting, sustained industry loss-leading may overbuild AI infrastructure beyond the long run equilibrium quantity of AI usage. The information environment in the sector regarding future demand for AI may be based on demand projections with current subsidized low prices, also leading to overinvestment. When the AI companies raise prices to achieve profitability, the realized demand may be less than what companies expect to supply, leading to a significant amount of wasted investment that could have been better purposed for other uses.

5. Open-source models will be a large component of future AI use for productivity tools

Rising costs of frontier AI models will make the cost advantage of the cheaper open-source models even more attractive to businesses. Due to having a more advantageous cost structure, it is likely that open-source models will supply a significant amount of demand for productivity tools not exposed directly to end consumers since businesses may be less sensitive to slightly worse model performance. Another advantage of open-source models is companies will be able to host it internally keeping proprietary data safe. The availability and usage of open-source models will supress profits for frontier AI model providers.

Conclusion

More research needs to be conducted to further understand industry dynamics in AI as it is critical for guiding investments and product development directions in the industry. While this brief sets forth a theoretical framework for the AI industry supported by evidence and observations of industry behavior, more empirical work is needed to estimate the price elasticity of AI products and the cost structures of AI companies. Furthermore, this theoretical framework can be combined with analysis of companies’ strategic positioning to project optimal strategies and paths for AI companies and investors. More qualitative and quantitative can be done to validate exactly why slop is unwanted and how quickly its value falls off in comparison to utility goods.

Acknowledgements

I would like to thank Jessica Mancini, Andrew Shi, Mei Torrey, Aina Nadeem, and Walker Wilson for their feedback and insights.

Claude Opus 4.7 and 4.8 was used to compile evidence and refine the theoretical framework based on my instructions. I reviewed all outputs of Claude with the original source and verified the accuracy of the charts, iterating towards the best version.

References

Artificial Analysis. n.d. “AI Model & API Providers Analysis.” Accessed May 25, 2026. https://artificialanalysis.ai.

Backlinko Team. 2026. “ChatGPT Statistics 2026: How Many People Use ChatGPT?” Backlinko, April 21. https://backlinko.com/chatgpt-stats.

Bawden, David, and Lyn Robinson. 2020. “Information Overload: An Introduction.” In Oxford Research Encyclopedia of Politics, by David Bawden and Lyn Robinson. Oxford University Press. https://doi.org/10.1093/acrefore/9780190228637.013.1360.

Béchard, Deni Ellis. 2026. “What Is the AI Compute Crunch, and Why Are AI Tools Hitting Usage Limits?” Scientific American, May 1. https://www.scientificamerican.com/article/what-is-the-ai-compute-crunch-and-why-are-ai-tools-hitting-usage-limits/.

Google Business. 2026. “Ads in AI Mode.” May 13. https://business.google.com/us/accelerate/announcements/ads-in-ai-mode/.

Hoffman, Benjamin. 2024. “First Came ‘Spam.’ Now, With A.I., We’ve Got ‘Slop.’” Style. The New York Times, June 11. https://www.nytimes.com/2024/06/11/style/ai-search-slop.html.

Jin, Berber. 2026. “OpenAI Scraps Sora Video Platform Months After Launch — 3rd Update.” Dow Jones Institutional News (New York), March 24. 3321145307. ProQuest Central. https://dartmouth.idm.oclc.org/login?url=https://www.proquest.com/wire-feeds/openai-scraps-sora-video-platform-months-after/docview/3321145307/se-2?accountid=10422.

Kayman, Alexa, and Etienne Segal. 2025. “Report: Midjourney Business Breakdown & Founding Story.” Contrary Research, May 23. https://research.contrary.com/company/midjourney.

Proton. 2026. “ChatGPT Ads Are Coming: What It Means and What You Can Do.” January 21. https://proton.me/blog/chatgpt-ads.

Smith, Dave. 2025. “OpenAI Says It Plans to Report Stunning Annual Losses through 2028—and Then Turn Wildly Profitable Just Two Years Later.” Yahoo Finance, November 12. https://finance.yahoo.com/news/openai-says-plans-report-stunning-161814899.html.

The Economist. 2024. “What Could Kill the $1trn Artificial-Intelligence Boom?” The Economist, July 28. https://www.economist.com/business/2024/07/28/what-could-kill-the-1trn-artificial-intelligence-boom.

vlogbrothers. 2026. What Is “Slop” (and Why It Gives Me Hope). 11:49. https://www.youtube.com/watch?v=dT5IJExTUR4.

[1] While some final goods can be used in the creation of other goods (a frying pan is a final good that is used to produce a meal), economists generally consider how a good is used and by whom. If a frying pan is purchased by a chef and used in a restaurant to perform his duties, then it is a capital good. But if it is purchased by a regular consumer for personal use, it is a final good. Similarly, Google’s AI for search is primarily used by consumers for personal purposes and can be considered generally a final good. Employees who need a research tool for their work may generally opt for a more advanced tool, such as deep research, or look much beyond the AI summary. Claude Code or Cowork is typically used by employees, including self-employed people, for accomplishing a business objective making it a capital good.